Solid foundations

The housing market has started the year with renewed momentum, following a quieter close to 2025. Greater mortgage choice and rates lower than those seen last year are helping to support growing confidence in the market.

Interest rates held

Consumer price inflation eased to 3.0% in January, down from 3.4% in December¹, which had marked the first increase after five consecutive months of decline, signaling that the broader downward trend has now resumed. Interest rates were maintained at 3.75% in February, a decision widely expected by economists given the mixed economic backdrop. However, rates are expected to lower over the year with one or potentially two further 0.25 percentage point cuts are expected. Whilst economic growth is expected to be modestly weaker over 2026 (at 1.1%)² this is close to the level that has historically been sufficient to drive positive house price growth.

Mortgage rates continue to ease

Mortgage product choice increased in January to 7,158 options, the highest total since October 2007³. The number of deals available to borrowers with 5% or 10% deposits has also reached an 18-year high, offering a welcome boost for first-time buyers looking to step onto the property ladder. Alongside greater choice, mortgage rates are easing with the latest five-year fixed rate falling to 3.95% - the first time it has been below 4% since September 2022⁴. Lower mortgage rates are helping to fuel the desire to move, while the easing of stress-testing requirements and expectations of further rate cuts are also reducing affordability pressures for borrowers.

Market momentum

In January there were 94,680 transactions, 1% lower than the same month last year. Transaction levels over 2025 were in line with the 10-year average of 1.2 million a year, a pace expected to continue throughout 2026⁵. Demand at the start of 2026 broadly mirrors 2024 levels but is around 9% lower than the busy start to last year, when buyers rushed to beat the April stamp duty deadline⁶. Mortgage approvals totalled 61,013 in December, down year-on-year, but above end-2023 levels of around 52,000⁴. Looking ahead, expectations of easing interest rates and a high level of choice should support renewed confidence across the market.

¹ Office for National Statistics, ² HM Treasury Average of Independent Forecasts,³ Moneyfacts, ⁴ Bank of England, ⁵ HMRC, ⁶ Zoopla

Rental market outlook

Rents across the UK remain 2.4% higher year on year, despite recent short-term softening¹. On a monthly basis, average rents fell by 1.1% in January to £1,302, the third consecutive monthly decline in line with a typical seasonal slowdown. Most regions saw small monthly decreases, with only the North West and South East avoiding falls. However, RICS data indicated a modest pick-up in tenant demand in January, ending two consecutive quarters of flat or slightly negative readings. In line with this, a net +28% of respondents expect rental prices to rise in the near term, up from +16% previously².

Renters’ Rights Reform

The Renters’ Rights Act brings major changes in England beginning to take effect from 1 May 2026. Described as the most significant reform to renting in a generation, it abolishes Section 21 “no-fault” evictions and introduces rolling periodic tenancies to improve stability for tenants, alongside a ban on rental bidding wars and stronger requirements for evidence-based rent increases. Further measures will be phased in over time, including a new Private Rented Sector Ombudsman and a national landlord database.

Supply boost

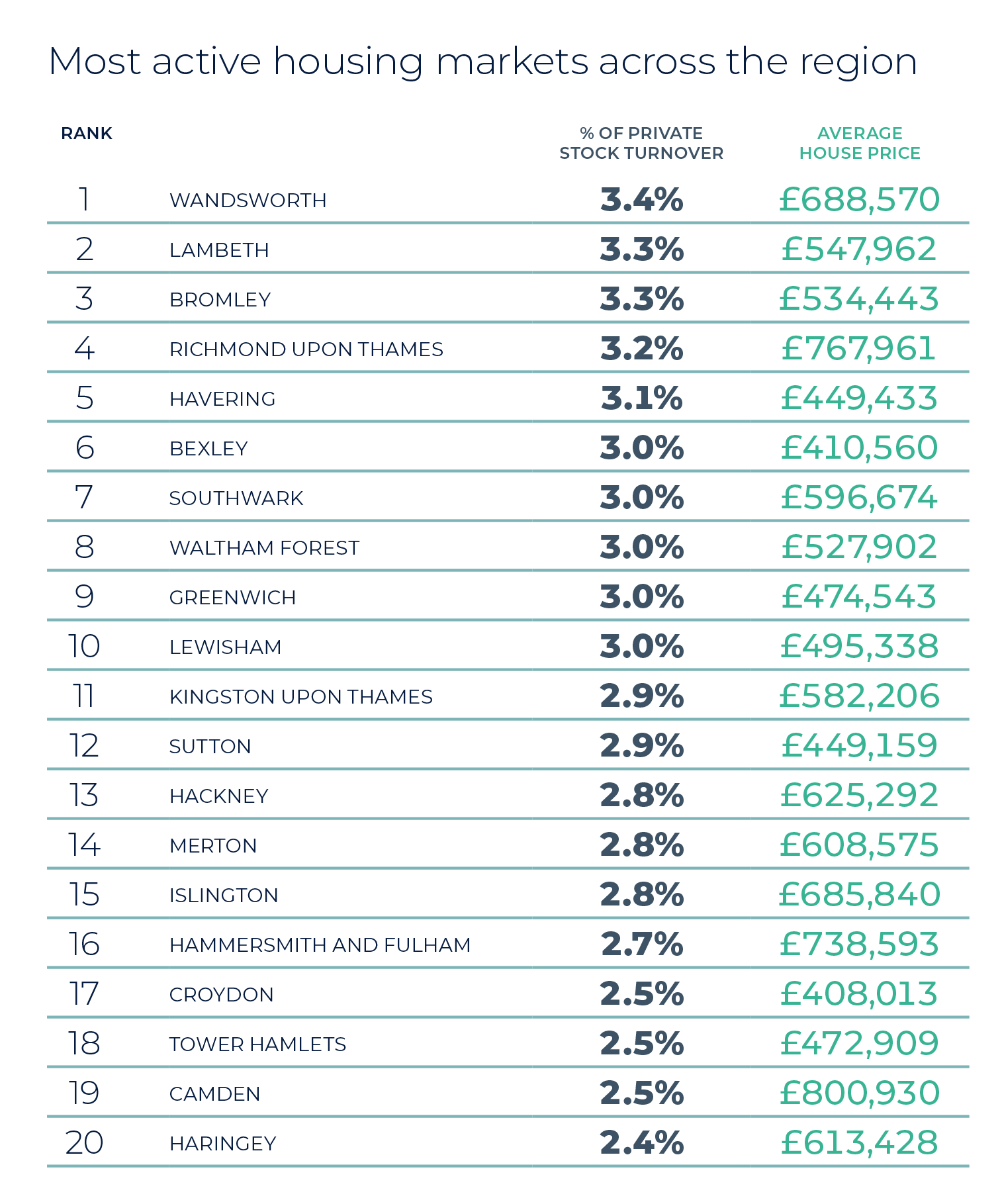

2026 began with the highest level of homes for sale in over eight years, with the average agent marketing 32 properties (Zoopla). Around a third of these homes were previously listed in 2025 and have since returned to the market after uncertainty late last year dampened activity. The uplift in supply is most pronounced in southern England, where listings in London were up 16% year on year and the South East saw a 9% increase. House price growth remains linked to supply, with increased availability moderating growth by giving buyers more choice and greater negotiating power. As always, local pricing can differ significantly from national trends. Average property values in the region softened 1.2% from last year’s levels. Strongest price growth was evident in Bromley (6.0%), slightly ahead of the next top performers Havering (5.2%) and Waltham Forest (4.0%).

Contact us

Sell your property with your local expert this season. Get a free instant online valuation.

The Guild is a UK-wide network of hand-selected independent estate agents across the UK. Whether you are buying, selling, letting or renting, explore where our Members are.

{kind=link}